Research Notes

Feb 04

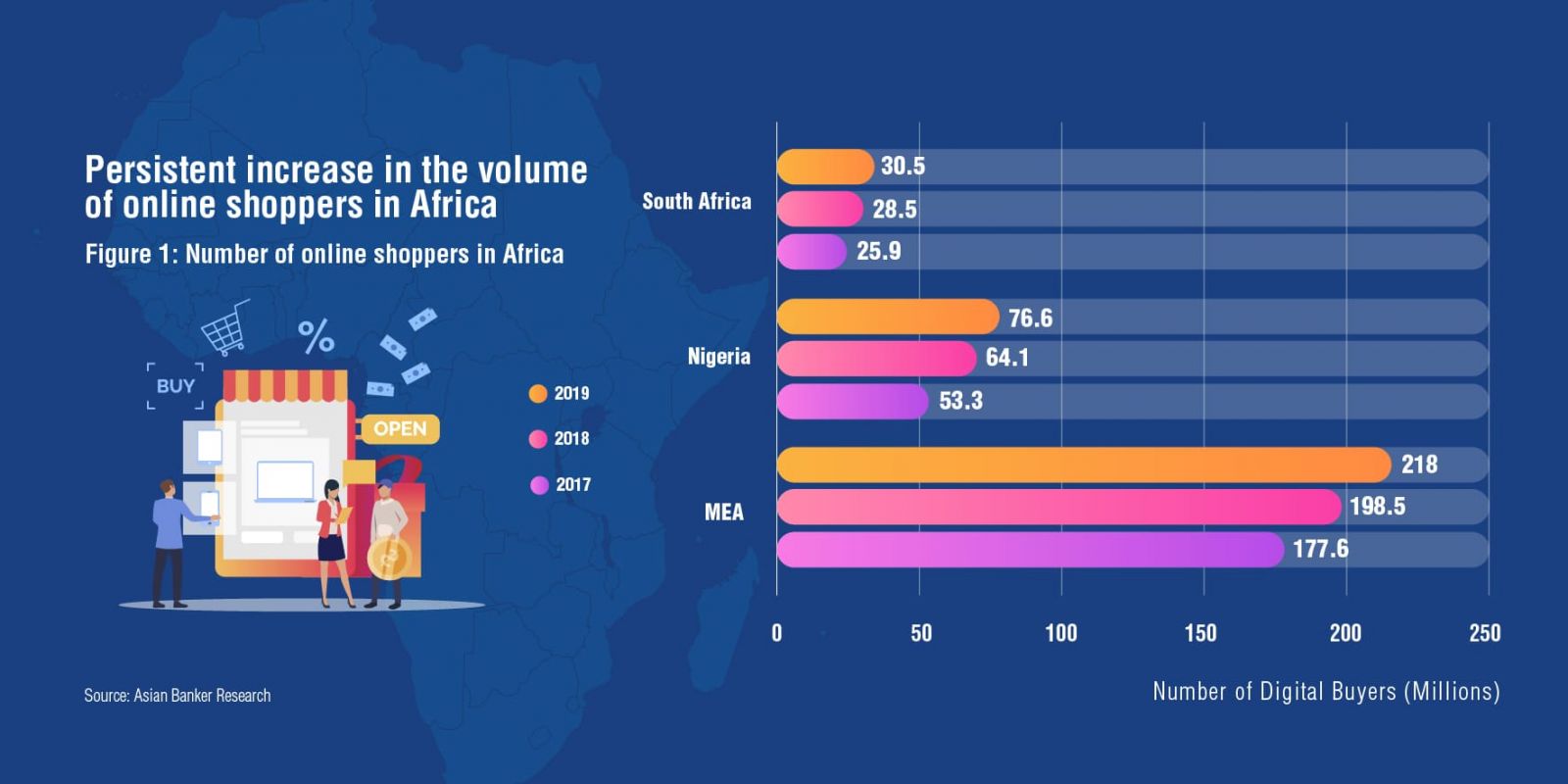

Africa’s e-commerce landscape is growing, with more players entering the industry. With increased e-payment innovations and technical security, Sub-Saharan Africa will continue to see growth in is number of online shoppers.